Adobe Stock: Strong Buy For This Software Leader (NASDAQ:ADBE)

1")

Jaap2/iStock Unreleased via Getty Images

In this analysis, we analyzed Adobe Incs (ADBE) Digital Media segment which consists of its Creative Cloud and Document Cloud businesses. We expect its Creative Clouds growth to continue, given its position as one of the most well-recognized creative softwares in the industry, as well as its comprehensive portfolio of software applications against competitors. Moreover, we expect its dominance in the PDF market with a first-mover advantage and effectively leveraging it to grow its massive user base to provide opportunities for growth through value-added feature subscriptions. Lastly, we determined that the company has a highly scalable business model, and we expect its revenue growth to continue outpacing its SG&A and R&D expense growth due to its solid branding and industry recognition, providing ample room for margin expansion.

Adobe

Most In-Demand Creative Software in The Market

Adobes Creative Cloud segment is the largest contributor to its Digital Media segments revenue representing 83.79% of the segment in FY2021. According to Research and Markets, the design, editing and rendering software market is $27.7 bln in 2020 and forecasted to grow at a CAGR of 5.6% through 2027. Based on its Creative Cloud revenue in 2020, this translates to a market share of 27.9% for Adobe.

A study by Venngage found that out of 100 job posts of graphic designers from Glassdoor, 76% of design jobs required Adobe Photoshop and 74% required Adobe InDesign and Illustrator. This highlights the industry recognition of Adobes creative software applications by creative professionals. According to the US Bureau of Labor Statistics, the employment of graphic designers is forecasted to grow by 3% until 2030.

Furthermore, there are various alternatives to Adobes creative software applications according to Just Creative, G2.com, MovieMaker and AppSumo Blog. Based on data from GetApp, we compiled the number of features of selected Adobes creative software products corresponding with each of its alternatives from a total of 33 competitors. The number of features of its competitors products ranges between 1 (FL Studio) and 55 (InVision).

We found that Adobe generally has a higher number of features than its competitors average. However, its competitors have a higher average number of features compared to Adobe XD and After Effects. Notwithstanding, Adobe has the broadest creative software portfolio as a whole with a total of 133 features for all selected creative software products combined and is higher than the total average features of all competitors. Thus, this implies that Adobe focuses on offering the widest breadth rather than specialization.

|

Adobe Creative Cloud |

Adobe Photoshop |

Adobe Illustrator |

Adobe XD |

Adobe Animate |

Adobe After Effects |

Adobe Audition |

Acrobat DC |

Total |

|

Adobe Number of Features |

24 |

16 |

26 |

21 |

8 |

17 |

21 |

133 |

|

Competitors Average Features |

13.8 |

12.3 |

29.2 |

16.0 |

18.0 |

14.2 |

21.0 |

125 |

Source: Just Creative, G2.com, MovieMaker, AppSumo Blog, GetApp

Thus, we believe that the comprehensiveness and feature-rich portfolio of creative software is an advantage to Adobe. In addition, it is recognized by employers as an essential skill in the creative industries. We believe that its comprehensive creative software applications portfolio could cement its position in the industry. Moreover, we believe that its strong industry recognition could provide an opportunity for it to gain market share as it only has a market share of 27.9%. We projected its Creative Cloud revenues based on its 4-year average growth rate of 23.03% tapering down by 5% as a conservative assumption followed by a forecasted design, editing and rendering software market CAGR of 5.6% through 2026.

|

Creative Cloud Segment Forecasts |

2017 |

2018 |

2019 |

2020 |

2021 |

2022F |

2023F |

2024F |

2025F |

2026F |

|

Creative Cloud ($ mln) |

4,174 |

5,343 |

6,482 |

7,736 |

9,550 |

11,272 |

12,741 |

13,764 |

14,535 |

15,349 |

|

Growth (%) |

28.01% |

21.32% |

19.35% |

23.45% |

18.03% |

13.0% |

8.0% |

5.6% |

5.6% |

Source: Adobe, Research and Markets, Khaveen Investments

Dominance In PDF Market Expected to Continue

Adobe created the PDF file format in 1993 which had become one of the most popular file formats. According to PDFAs chart below, the PDF format accounts for over 80% of file formats on the web. Among the benefits associated with PDF files is its format consistency and it can be opened across multiple operating systems and devices. Moreover, it supports security features such as allowing e-signatures and the ability to lock files and limit access.

2")

PDFA

In its Q4 2021 earnings briefing, the management disclosed that there are 2.5 bln mobile devices with a reader or Acrobat installed. Based on Gartner, the installed base of smartphones, desktops, tablets and laptops were 6.084 bln in 2020. This translates to 41% of the global installed base of electronic devices having Adobes PDF reader software installed.

Adobe Reader is free to download while the premium version with more features is available for a subscription fee. We believe that this is its strategy to give its software for free and upsell to its premium subscription to its massive installed base.

We believe that with its market dominance and strategy to charge premium subscription fees, Adobe has dominated the market with a market share of 76.8% based on the PDF editor software market of $1.95 bln in 2020 by Research and Markets with a CAGR of 8.68% by 2025. We forecasted its segment revenue based on its segment 4-year average revenue growth of 23.98% but tapering down by 5% as a conservative assumption followed by the market CAGR of 8.68% through 2026.

|

Document Cloud Segment Forecast |

2019 |

2020 |

2021 |

2022F |

2023F |

2024F |

2025F |

2026F |

|

Document Cloud ($ mln) |

1,225 |

1,497 |

1,970 |

2,344 |

2,672 |

2,912 |

3,164 |

3,439 |

|

Growth (%) |

24.75% |

22.20% |

31.60% |

18.98% |

13.98% |

8.98% |

8.68% |

8.68% |

Source: Adobe, Research and Markets, Khaveen Investments

Overall, we believe that Adobe has leveraged its first-mover advantage effectively to dominate and gain scale in terms of its users globally capturing 41% of the installed base of devices. In addition to that, we believe that its strategy to upsell features through premium subscriptions has allowed it to capitalize on its massive user base and dominate with a market share of 76.8%. We expect it to further capitalize on its advantage and stands to benefit from the growth of its PDF software segment.

Margin Growth Supported by Scalability of SG&A and R&D

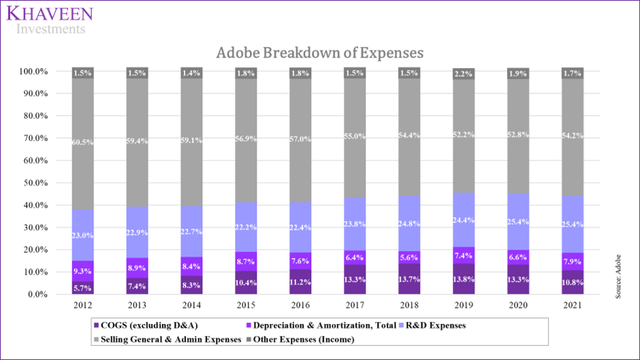

The company has had stable gross margins in the past 10 years at 86.3% and does not have inventory as a software company. However, net margins have grown considerably in the past 10 years from 18.91% in 2012 to 30.55% in 2021. As a software company, it instead focuses its expenses on R&D and SG&A. The companys SG&A and R&D expenses represent the majority of its total expenses at 79.6% of total expenses in 2021.

Adobe, Khaveen Investments

According to its annual report, the majority of the growth of selling and marketing expenses is from an increase in marketing expenses. In the past 10 years, its revenue growth outpaced its SG&A growth, its revenue growth/SG&A growth has a 10-year average at 1.08 (excluding 2015).

We believe that the companys revenue growth could continue to outpace its SG&A growth. Firstly, its creative software benefits from its wide recognition by the industry. Secondly, the company has strong branding as it is ranked 27 in the Best Global Brands 2020 and rose by 12 places. Moreover, it also benefits from its established network as a popular application. When searching for PDF readers on Google and app stores such as Google Play and the App Store, Adobe PDF reader appears first in the search results except for Microsofts app store.

We forecasted its SG&A expenses by applying an average 10-year revenue growth/SG&A growth of 1.08 with our revenue growth forecasts through 2026. All in all, we assume its SG&A as a % of revenue to decline from 34.2% to 33.1% in 2026.

Furthermore, we also believe that its margin upside could be provided by its revenue growth outpacing its R&D expenses, which have a revenue growth/R&D expense growth average of 1.62 in the past 10 years and slightly lower compared to SG&A. According to its annual report, its R&D expenses growth primarily stemmed from the increase of incentive compensation and base compensation. According to Capiche, software inflation was 62% between 2009 to 2019 whereas computer programmer wages increased by 24% in the same period.

Moreover, another reason for the scalability of software companies in terms of costs is due to the nature of software development where the initial development cost to produce the software is high but the development costs are fixed and can be spread out among its customer base leading to lower unit costs in the long run as explained in the following quote.

The high cost of developing complex software can be amortized over the vast number of users. If a web site like Amazon is currently worth a billion dollars, and it has 100 million users, the cost per user is only $10. Kurt Guntheroth, Software Engineer for 40 years

Similarly, we forecasted its R&D expenses by applying an average 10-year revenue growth/R&D growth factor of 1.16 with our revenue growth forecasts through 2026. All in all, we assume its R&D as a % of revenue to decline from 16.1% to 15.1% in 2026.

|

Adobe SG&A Forecast ($ mln) |

2020 |

2021 |

2022F |

2023F |

2024F |

2025F |

2026F |

|

Adobe Revenue |

12,868 |

15,785 |

18,296 |

20,571 |

22,383 |

24,032 |

25,830 |

|

Revenue Growth % (‘a’) |

15.2% |

22.7% |

15.9% |

12.4% |

8.8% |

7.4% |

7.5% |

|

SG&A |

4,559 |

5,406 |

6,201 |

6,913 |

7,476 |

7,985 |

8,537 |

|

SG&A Growth % (‘b’) |

10.5% |

18.6% |

14.7% |

11.5% |

8.1% |

6.8% |

6.9% |

|

Revenue Growth/SG&A Growth (‘c’) |

1.44 |

1.22 |

1.08 |

1.08 |

1.08 |

1.08 |

1.08 |

|

SG/A as % of Revenue |

35.4% |

34.2% |

33.9% |

33.6% |

33.4% |

33.2% |

33.1% |

|

R&D |

2,188 |

2,540 |

2,889 |

3,199 |

3,443 |

3,662 |

3,898 |

|

R&D Growth % (‘d’) |

13.4% |

16.1% |

13.7% |

10.7% |

7.6% |

6.4% |

6.5% |

|

Revenue Growth/R&D Growth (‘e’) |

1.14 |

1.41 |

1.16 |

1.16 |

1.16 |

1.16 |

1.16 |

|

R&D as % of Revenue |

17.0% |

16.1% |

15.8% |

15.6% |

15.4% |

15.2% |

15.1% |

*b = a/c

*d = a/e

Source: Adobe, Khaveen Investments

Overall, we believe that the companys margins could continue to increase through 2026 due to the scalability of its business model. As one of the most recognized creative software providers by employers as well as a prominent branding as highlighted by its awards and popularity as the leading search result in search engines and app stores, we believe that its revenue growth could scale higher than SG&A growth. Furthermore, we also believe its R&Ds scalability could provide additional upside to its margins.

Its average gross and net margins are 86.6% and 29.95% respectively for the past 5 years. The margins have been improving with its revenue growth.

Adobe, Khaveen Investments

Risks: Competition from Free Creative Software Startups

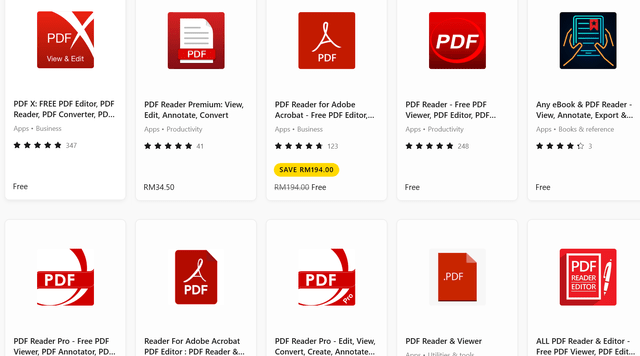

As a software company, it competes against various competitors in an industry with low barriers to entry with an asset-light business model. In the creative software market, there are various paid and free creative software from competitors. While it has the most comprehensive set of software applications, companies may create or replicate similar competing solutions to enhance their software or build up their portfolio to challenge Adobe. In addition, there are various paid and free PDF readers in the market competing against Adobe Acrobat and Reader as seen in the chart below. As highlighted, we believe it adopts a strategy to provide its PDF software as free initially and upsell value-added features through subscriptions. However, we believe that the intense competition from free PDF readers limits its pricing power to change its strategy to charge a fee for the initial download, which may affect its ability to monetize its platform.

Microsoft Store

We believe the company operates in an industry with very low bargaining power over customers which limits its pricing power and its growth potential by raising prices for its products. If it raises its prices, we expect customers to easily switch to free alternatives.

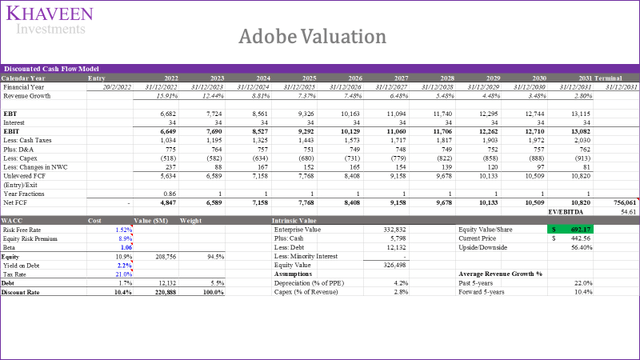

Valuation

To value the company, we used a DCF valuation as we expect the company to have positive FCFs and based its terminal value on the selected software companies’ average EV/EBITDA of 54.61x.

Seeking Alpha, Khaveen Investments

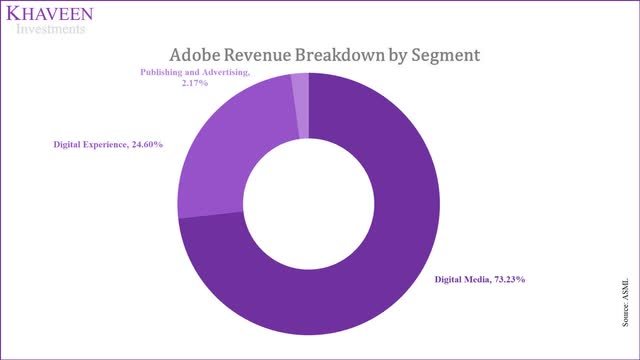

We forecast Adobes revenue by its business segment in the table below. We project its Digital Media revenue growth by two main divisions. i.e., Creative Cloud and the Document Cloud. For the first three years, we applied a 4-year average revenue growth and tapered it down by 5%, followed by the design, editing, and rendering software market growth of 5.6% and PDF editor market growth of 8.68% respectively till 2026. We forecast the Digital Experience segment to grow at the global customer relationship management market growth rate of 12.1%. We applied a 3-year average revenue growth of -13.5% for the Publishing and Advertising segment.

|

Revenue Segments ($ mln) |

2019 |

2020 |

2021 |

2022F |

2023F |

2024F |

2025F |

2026F |

|

Digital Media |

7,707 |

9,233 |

11,520 |

13,616 |

15,412 |

16,675 |

17,699 |

18,788 |

|

Growth (%) |

21.85% |

19.80% |

24.77% |

18.19% |

13.19% |

8.20% |

6.14% |

6.15% |

|

Digital Experience |

2,795 |

3,125 |

3,870 |

4,338 |

4,863 |

5,452 |

6,111 |

6,851 |

|

Growth (%) |

34.83% |

11.81% |

23.84% |

12.1% |

12.1% |

12.1% |

12.1% |

12.1% |

|

Publishing and Advertising |

669 |

510 |

395 |

342 |

296 |

256 |

221 |

191 |

|

Growth (%) |

5.85% |

-23.77% |

-22.55% |

-13.5% |

-13.5% |

-13.5% |

-13.5% |

-13.5% |

|

Total |

11,171 |

12,868 |

15,785 |

18,296 |

20,571 |

22,383 |

24,032 |

25,830 |

|

Total Growth % |

23.7% |

15.2% |

22.7% |

15.9% |

12.4% |

8.8% |

7.4% |

7.5% |

Source: Adobe, Fortune Business Insights, Khaveen Investments

Based on a discount rate of 10.4% (companys WACC), our model shows the company’s shares are undervalued by 56%.

Khaveen Investments

Verdict

We analyzed Adobes Digital Media segment in terms of its Creative Cloud and Document Cloud businesses. For its Creative Cloud, we highlighted its creative software applications’ strong recognition and demand in the industry and its comprehensive software portfolio with a superior set of features combined compared to alternatives. Moreover, we highlighted its PDF reader software market dominance leveraging its first-mover advantage and a massive user base of 41% of the global installed base of devices with a strategy to offer free installation and then upsell premium subscription features. Lastly, we highlighted the scalability of its business model with SG&A and R&D expenses expected to continue outpacing revenue growth due to its strong branding and industry recognition. Overall, we rate the company as a Strong Buy with a target price of $692.17.